PP124

Capital Calls in Real Estate Syndications (And What to Do)

For most of the last decade, the idea of a capital call was mostly theoretical, especially in real estate syndications.

Interest rates kept getting lower, values kept getting higher, and very few deals experienced any meaningful distress. The capital call section of a syndication’s PPM and operating agreement got skimmed (if read at all) and was never thought of again – almost no passive investor actually experienced one.

That era is decidedly over.

Capital call notices are landing in investor inboxes, particularly for 2021- and 2022-vintage multifamily deals that got done at the peak of the market. And unfortunately, most investors opening them have no idea what happens next or how to decide what to do.

Hopefully you’re never in a deal with a capital call – but if one ever shows up in your inbox, here’s a high-level framework for how to approach it.

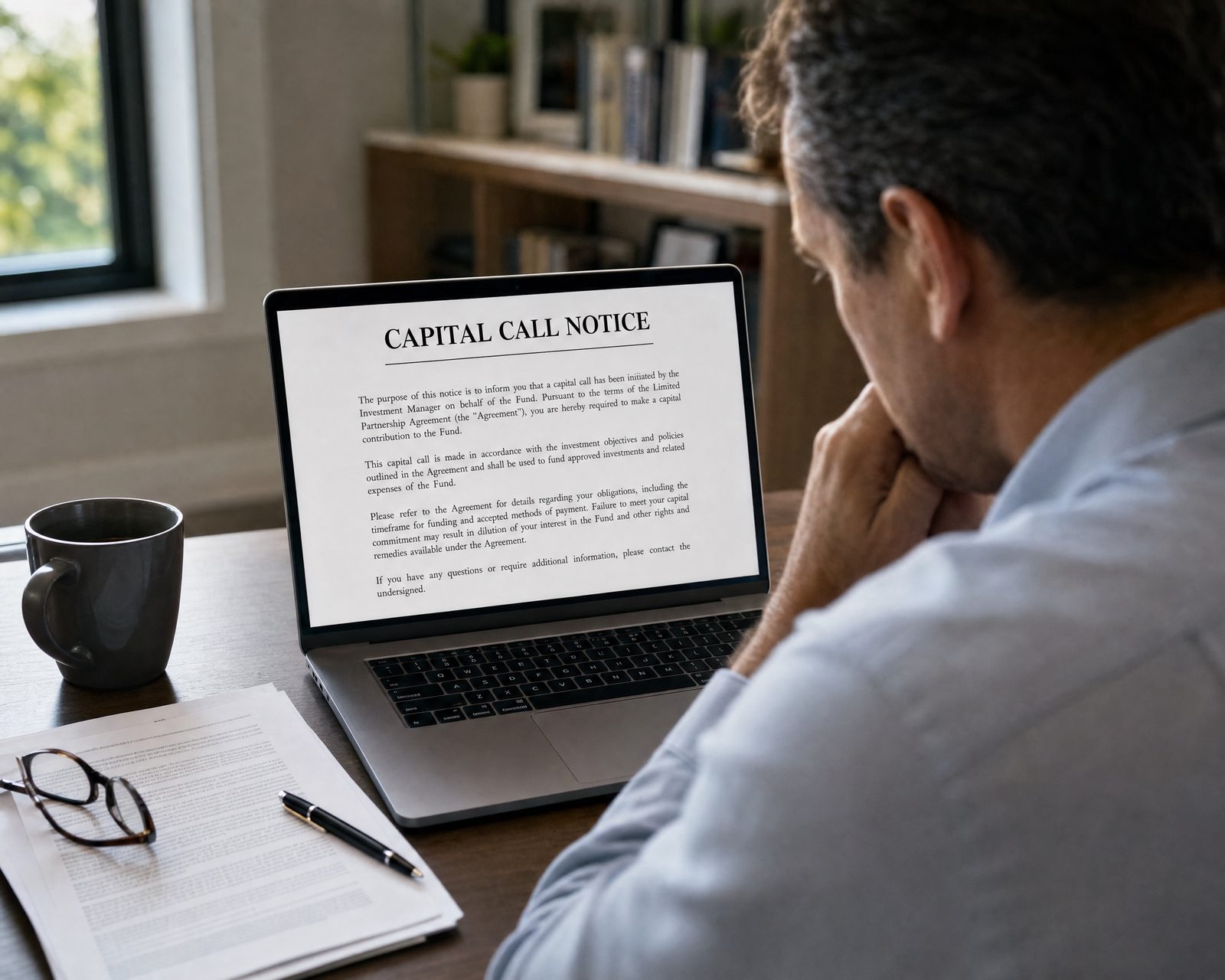

What a capital call actually is

A capital call is simply a demand for additional money in an investment. And in some parts of the investing world, it’s routine and benign.

Private equity and venture funds call capital in planned tranches: you commit to a total number up front and they ask for parts of it over time. That’s the design.

And while you can find that same system in some real estate funds or syndications, it’s far less common.

A syndication usually takes your full investment on day one. So if a capital call shows up later, it almost always means something went off-plan. In most syndications, a capital call is a distress signal, not a pre-scheduled event.

Why we’re seeing them now

Most of today’s capital calls trace back to cheap debt from 2021 and early 2022 colliding with a high-rate world.

Operators on floating-rate loans bought rate caps to limit their exposure to rising interest (smart). Those caps were cheap when rates were low – renewing them has, in some cases, cost more than 35x the original price. So they’re trapped…they either need cash to fund the rate cap purchase, or cash to service higher debt payments.

Others used fixed-rate debt but on typical CRE term lengths, often five years. Those loans are now maturing into higher rates and flat-to-shrinking NOI – the property won’t support the same loan balance, and refinancing means bringing cash to the table (a “cash-in” refi).

Either way, lenders want paydowns, debt costs more, and operating costs have climbed too. So many operators need more cash to just keep their deal afloat.

What’s unique to your deal

So the operator needs more capital, and turns to investors.

What that call can actually do to you is set almost entirely by your own paperwork – and it comes down to two questions.

First, is participation optional or mandatory? Most syndication capital calls are technically optional, meaning you can decline. But some operating agreements make them binding, meaning that a sponsor could pursue legal action to collect.

Second, what happens if you don’t participate? Depending on what your OA spells out, declining could:

- Dilute your ownership (sometimes on punitive terms that give those who participate even more of the deal)

- Subordinate or suspend your preferred return

- Put new “member loans” ahead of you for any future distributions.

And in the harshest documents, your interest can be force-sold at a steep discount.

To reiterate, none of that is automatic and the specific details will vary from deal to deal. Which underscores the importance of a boring task: read your deal docs, and know what they say before you’re staring at a notice.

How to decide whether to participate

But even when there are “penalties” for not participating, writing a new check isn’t always the smart decision.

A capital call exists to fix a specific problem – so start with what the money is actually for and whether it plausibly solves it.

Then, forget how much you’ve already put in (it’s spent no matter what you decide now) and ask one question: knowing what you know about this deal today, would you invest the called amount into it from scratch?

Some sponsors issue capital calls as a last-ditch effort, and the money often won’t fix what’s actually broken. The penalties are built to make “yes” feel forced (”pay or lose everything”) – but if the rescue won’t hold, your original investment is likely gone regardless.

So pressure-test the deal:

- Is this the first call, or one of several?

- Does this money fix the issue, or just buy a few months?

- Is the problem a passing headwind or structural mismanagement?

- Is there a realistic path to clear the capital stack and actually return investor money?

Sometimes the answers are good, and funding the call is the smart move.

Sometimes the disciplined call is to take your loss and refuse to throw good money after bad. And if the call is optional, walking away caps that loss at the money you already invested.

Before the notice arrives

Capital calls aren’t rare anymore – but being blindsided by one is a choice.

Almost everything that determines your right answer is knowable today, before any notice lands. So if you think you’re in a deal that might be looking at a capital call, do three things now:

- Find out which kind of call your documents allow

- Determine what declining would cost you

- Write down the questions you’d ask to judge if a rescue is worth funding

You may never get a capital call. But if you do, it’s a real decision under a deadline with real money on the line – a decision where a little preparation can make a lot of difference.

Want to know exactly what your deal docs say about a capital call without spending hours pouring over them? Here’s a prompt you can paste into ChatGPT or Claude along with your PPM and operating agreement:

I've attached the private placement memorandum and operating agreement for a real estate syndication I'm invested in as a passive limited partner. Walk me through the capital call and default provisions in plain English.

Specifically:

(1) Can the sponsor require additional capital, and is a call optional or mandatory?

(2) Is there a cap on how much can be called, or does any call need investor consent?

(3) Exactly what happens to my ownership, preferred return (if there is one), and distribution priority if I decline to participate?

(4) Are there member loans, dilution penalties, or forced-sale provisions, and how do they work in the context of a capital call?

(5) What notice and cure window do I get?Quote the relevant section for each answer, and flag anything that looks unusually aggressive compared to typical syndication terms.

Found this valuable? Join hundreds of sophisticated investors and receive these insights direct to your inbox every week.